Part Two: Scope 3 Planning using Life Cycle Assessment (LCA)

Author: Steve Bows, Certified Master Anaplanner and Managing Director, Zooss Consulting.

In Part 1 of this series, we learned the difference between Scope 1, Scope 2, and Scope 3 carbon emissions, and how we could incorporate energy use data (fossil fuels burnt and electricity consumed) to determine our Scope 1 and Scope 2 emissions. We also learned that Scope 3 emissions are larger, and harder to identify than Scope 1 and Scope 2.

Just to recap, Scope 3 emissions represent ‘embodied carbon’ in a company’s supply chain — both upstream and downstream. A good example is concrete manufacturing, which uses cement as its main ingredient. Cement production (one step upstream in the concrete manufacturer’s supply chain) is very carbon intensive — in this case, it is not the burning of fossil fuels, but rather the heating of limestone that produces carbon dioxide as a natural chemical reaction. These are Scope 1 emissions for the cement producer, but Scope 3 emissions for the concrete manufacturer that buys the cement.

There are two approaches to measuring Scope 3 emissions: Life Cycle Assessment (LCA) and Input Output Analysis (IOA). Getting a complete picture requires combining the two together, which we will discuss in the third article of this series. For now, let’s focus on the ‘bottom-up’ approach to emissions measurement, the LCA, and see how we can use the data it produces in our Anaplan models.

Introducing Life Cycle Assessment (LCA)

LCAs are studies conducted by specialist consultants (typically environmental engineers) which attempt to quantify the environmental impact of specific production processes. The LCA approach was first standardized as a Code of Practice in the 1990s by the Society for Environmental Toxicology and Chemistry (SETAC), which gives you an idea of the areas of concern it was originally designed to address (toxic waste, essentially). This was later taken up by the International Standards Organisation in ISOs 14040 and 14044, which in turn has been further refined, most notably for our purposes in a standard developed specifically for measuring carbon emissions, PAS 2050 (1).

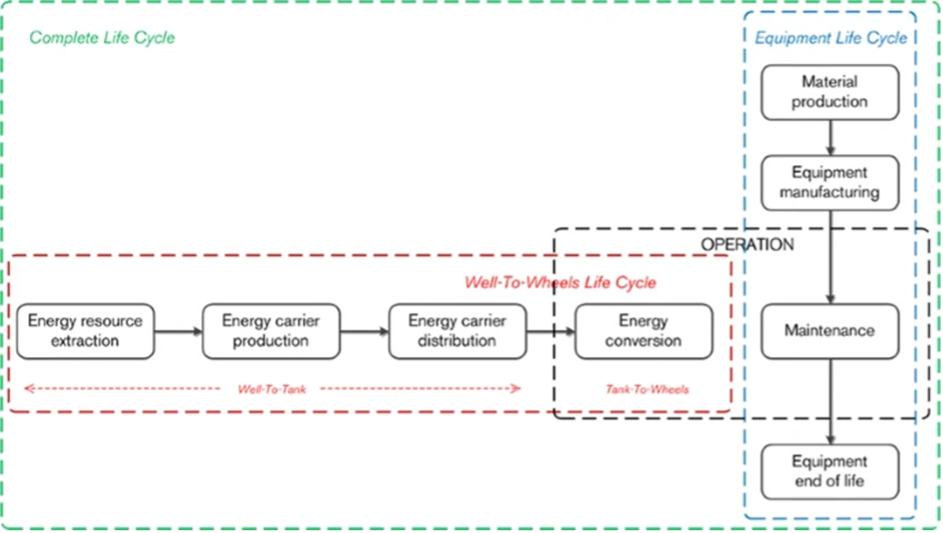

So how does it work? First, you need to define what ‘life cycle’ means — the scope of the LCA study. This means making some tough decisions about boundaries, both in terms of the product/process being studied, and also how far upstream and downstream you will measure. LCAs are resource intensive, so you would tend to focus on answering a specific question, such as “will I reduce carbon emissions (of all 3 scopes) if I swap my petrol vehicle fleet to battery electric vehicles?” To answer that question, you would look at a complete life cycle diagram of the vehicle, such as the one below, and decide whether the well-to-wheels life cycle or the equipment life cycle is the most important. If there is no material difference in certain stages of the life cycle for the options you are analyzing, then it probably doesn’t make sense to include those stages in your scope.

For instance, in comparing petrol to battery electric vehicles, we would expect the petrol vehicle to have higher emissions in the well-to-wheels life cycle (mostly Scope 1 from burning fuel, but also some Scope 3 from the well-to-tank extraction and transportation processes of getting the petrol to the car in the first place). However, the battery electric vehicle will have a higher carbon footprint from the equipment life cycle, due to the extraction and refinement processes for the materials that make up its battery (we expect the rest of the chassis to be much the same between the two options).

So the answer to our question is probably “it depends on how much the vehicles are used” since the Scope 1 emissions of petrol are variable per km traveled, whereas the Scope 3 (embodied) emissions of the battery electric vehicle are fixed at the point of purchase.

How can we use LCA data in Anaplan?

This is an example of how an LCA works, and why it might be commissioned, but how can we use this data in Anaplan? Well, there are two obvious use cases:

- Scenario planning: LCA studies are generally framed as a choice between two or more options, to enable a business decision to be made. In the example above, the LCA cannot provide a definitive answer, because it is missing a key business variable (kms traveled). A scenario planning model enabling users to develop what-if scenarios for different sections of their vehicle fleet by varying kms traveled assumptions would provide the missing link.

- Extended Bill of Materials (BOM): LCAs measure emissions per ‘functional unit,’ which is defined at the outset of the study. In the example above, it would probably be something like ‘per 1,000kms traveled.’ But for a product-based LCA, for example, analyzing the emissions footprint of beer

(2), the functional unit might be a hectolitre (hL), which is 100 liters. In this case, we would expect the LCA to tell us the carbon emissions ‘yield’ (kgCO2e/hL) for each stage of the beer-making process that it covers. We can easily insert this into our BOM (we just need to convert the functional unit to our BOM Unit of Measure) and have the emissions footprint flex in line with our production plan.

The limitations of LCA data

Hopefully by now you are super excited about how you might use LCA data to augment your project and production planning models, but before you run off searching for LCAs, it is a good idea to consider some of the limitations.

Most importantly, there are business scope limitations. As I mentioned earlier, LCAs are resource intensive, so even if you find one that you can use, it may not cover all the products and processes that you’re interested in. The priorities of the sustainability team may not match the priorities of the planning team.

Secondly, there are life-cycle stage limitations. An LCA is unlikely to give you a complete upstream and downstream assessment because supply chains are many levels deep and it would require the LCA team to visit your suppliers, then the suppliers of your suppliers, and so on, to give a full upstream assessment.

Some of these limitations are catered for by using secondary data from published Life Cycle Inventories (for example, the LCA team can look up the average carbon footprint of a 20-ton truck per km traveled and kg carried, rather than measuring it themselves), but secondary data is less accurate, and will never completely eliminate the boundary problem.

Solving boundary problems with Input Output Analysis

These boundary problems are an inherent feature of LCAs, which only measure a finite set of data in what is often an infinite supply chain. Input Output Analysis (IOA) can be used to attribute footprint values to the remainder of the supply chain that has not been measured directly, using some very clever maths. In the final (next) article of the series, we will explore IOA (specifically Environmentally Extended IOA), and talk about how you might go about incorporating the results of IOA in your Anaplan models.

Summary

In the first article of this series, we looked at the difference between Scope 1, Scope 2 and Scope 3 emissions, and how you might incorporate Scope 1 (direct) and Scope 2 (electricity-based) emission planning in your Anaplan models. In this article, we have looked at how Life Cycle Assessment data can be used to parameterize planning models that address Scope 3 (embodied carbon) as well.

If you’ve found this article useful, watch this space for the third and final article in the series, where we discuss Input Output Analysis, and how it can be used to solve the boundary problems inherent in the LCA approach for Scope 3 planning.

And finally, I am conscious that I have covered a lot of ground quite quickly in this article, so please leave a comment if you have any questions about LCAs, or ideas for use cases beyond the ones I’ve mentioned here. This is an emerging field, so there are no right or wrong answers!

------------------

(1) Source: https://www.en-standard.eu/pas-2050-2011-specification-for-the-assessment-of-the-life-cycle-greenhouse-gas-emissions-of-goods-and-services/

(2) I’m not suggesting that this should be combined with driving your battery-electric vehicle!